Long-term care insurance is an important financial tool that helps individuals cover the cost of extended care services, including nursing homes, assisted living facilities, and in-home care. The Federal Long-Term Care Insurance Program (FLTCIP) is a specific plan designed for U.S. federal employees, retirees, and eligible family members. This guide explains how the program works, who qualifies, common pitfalls to avoid, and what to consider before choosing a provider.

What is Federal Long-Term Care Insurance?

The Federal Long-Term Care Insurance Program (FLTCIP) provides long-term care coverage to federal employees, U.S. Postal Service workers, members of the uniformed services, and eligible relatives. It helps cover services that are typically not included in standard health insurance, Medicare, or Medicaid, such as assistance with daily living activities or long-term facility stays.

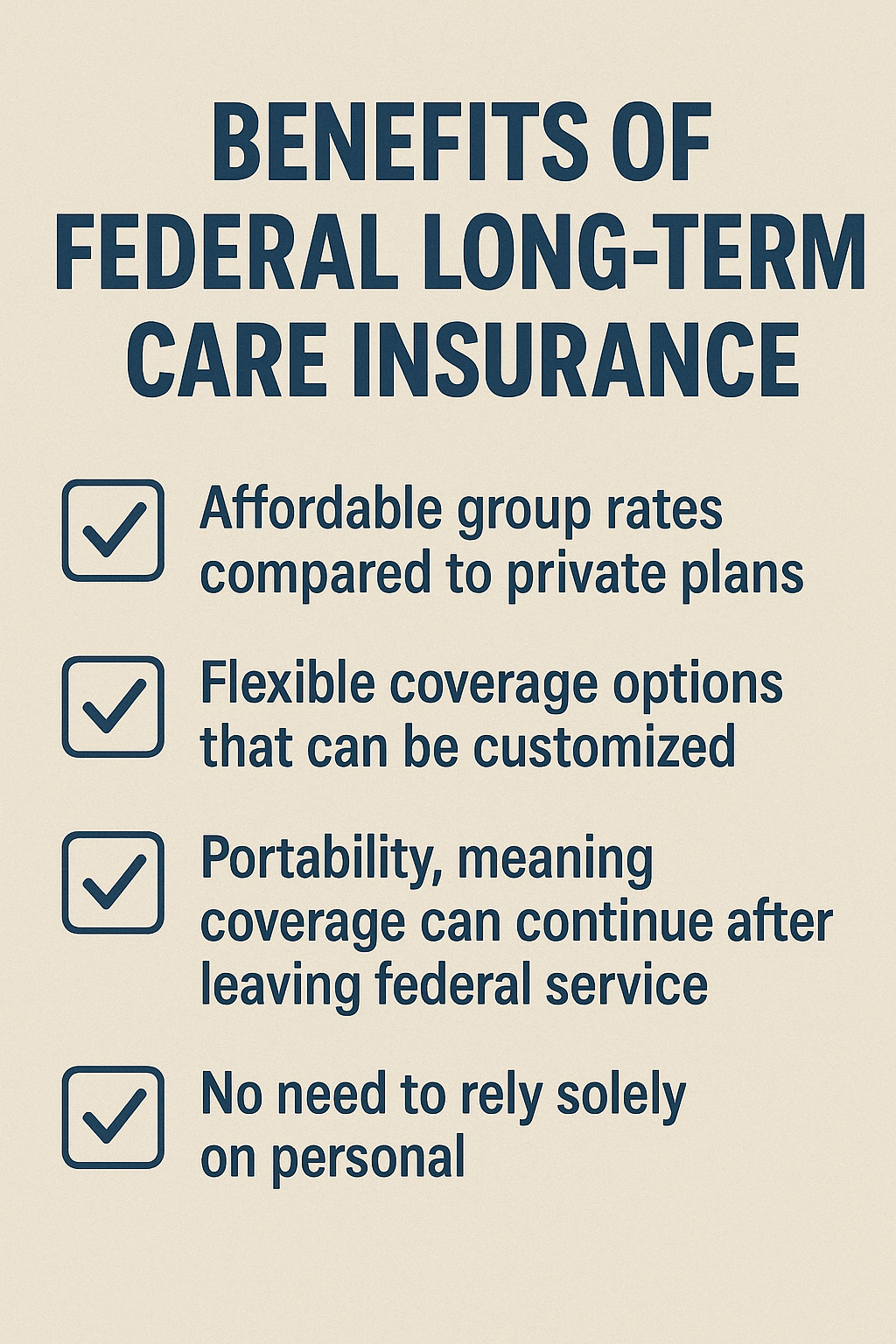

Benefits of Federal Long-Term Care Insurance

1. Affordable group rates compared to private plans.

2. Flexible coverage options that can be customized.

3. Portability, meaning coverage can continue after leaving federal service.

4. No need to rely solely on personal savings or Medicaid.

What Disqualifies You from Long-Term Care Insurance?

Certain medical and cognitive conditions may disqualify you from obtaining long-term care insurance. These can include:

– Alzheimer’s disease or other forms of dementia

– Parkinson’s disease in advanced stages

– Severe mobility limitations

– Chronic illnesses that require constant supervision

Applicants usually undergo a health screening process. If you already require assistance with activities of daily living, you may not qualify.

CNA Long-Term Care Insurance

CNA is a major private long-term care insurance provider that offers a variety of plans. However, customer reviews are mixed. While CNA offers flexible options, some policyholders have reported slow claims processing and communication issues. Comparing CNA with the Federal Long-Term Care Insurance Program can help you make an informed decision.

Worst Long-Term Care Insurance Companies

While many companies offer long-term care insurance, not all have good reputations. Common red flags include excessive premium increases, poor customer service, and delayed claim approvals. Before committing, check independent reviews, financial strength ratings, and consumer complaint data.

How to Choose the Best Long-Term Care Insurance Plan

1. Compare premiums and coverage details.

2. Check the financial stability of the insurer.

3. Review claim approval timelines and customer feedback.

4. Consider whether you need inflation protection.

5. Evaluate your current health status and family medical history.

Final Thoughts

Federal long-term care insurance can be a valuable safety net, especially for those in the federal workforce. However, it’s essential to weigh the pros and cons, understand what could disqualify you, and compare private options such as CNA. By doing thorough research, you can choose a plan that pro

While the Federal Long-Term Care Insurance Program (FLTCIP) was primarily designed for federal employees, postal workers, and retirees, its growing popularity has made it a benchmark for understanding long-term care across the United States. The program allows individuals to plan ahead for potential healthcare expenses that are often not covered by Medicare or traditional health insurance — such as extended nursing home care, assisted living, or in-home health support.

One of the key strengths of Federal Long-Term Care Insurance is flexibility. Policyholders can choose customized coverage options that fit their health needs, age, and budget. For example, you can select daily benefit amounts, waiting periods, and inflation protection features to ensure your plan remains valuable over time. This level of control helps individuals protect their retirement savings and maintain financial independence, even if long-term care becomes necessary later in life.

In 2025, as healthcare costs continue to rise, more Americans are realizing the importance of early financial planning. The federal government’s long-term care initiative not only offers affordable coverage but also promotes awareness about the real costs of aging. By investing in a solid long-term care plan today, federal employees and retirees can secure peace of mind — knowing their future care needs won’t create a financial burden for their loved ones.

CLICK HERE FOR: Final Expense Insurance in the USA: Complete Guide for 2025

The U.S. Office of Personnel Management manages the Federal Long-Term Care Insurance Program for eligible employees and retirees.

[…] Click her for :Federal Long-Term Care Insurance: Everything You Need to Know […]